How much Bitcoin to retire by 2030 and the risks

Analysts say 2–5 BTC could generate about $100,000 a year by 2030, depending on price and withdrawal rules, as public pensions increase exposure amid warnings of steep volatility.

Analysts estimate an investor would need roughly 2 to 5 BTC to produce about $100,000 a year by 2030, with the final number depending on future price levels and the withdrawal rate an investor uses. Projections vary widely across major price forecasts and retirement models.

Forecasts cited by market participants range from mid-five-figure valuations in the near term to seven-figure targets longer term. Matthew Sigel, head of digital assets research at VanEck, has described $1 million per Bitcoin as the firm’s base case by 2031. Other firms place Bitcoin between $120,000 and $250,000 by the end of 2026. Long-range projections from some investors include $1 million and $1.2 million targets in coming years. Using the conventional 4% withdrawal rule, an investor seeking $100,000 a year would need about $2.5 million in assets; at $500,000 per coin that equates to roughly five BTC. More aggressive withdrawal models discussed at recent industry conferences propose 6% to 8% rates, which would reduce the number of BTC required for the same annual income in simulation examples.

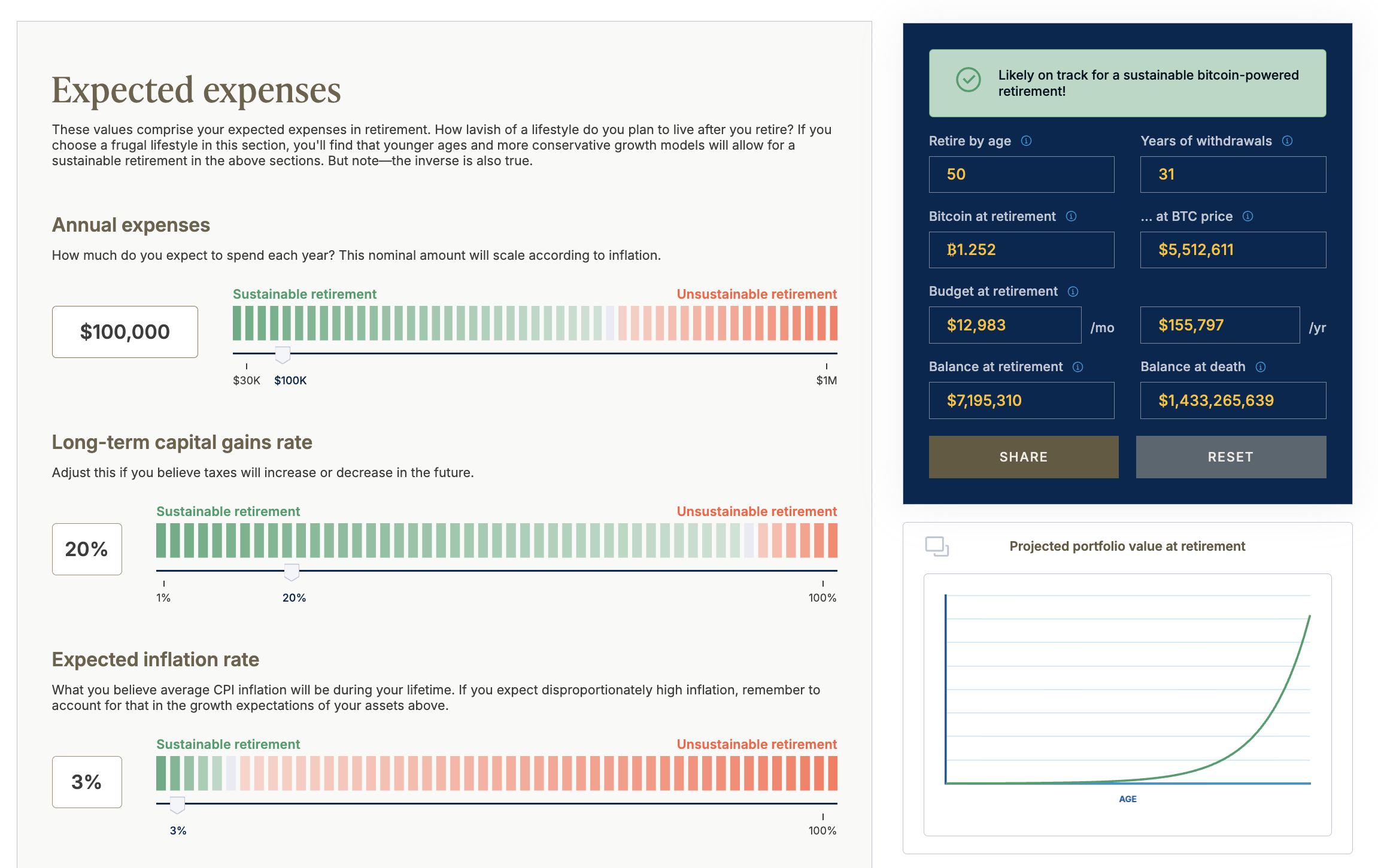

Online calculators let savers test different scenarios. Tools such as a Bitcoin retirement calculator from custody and planning services allow users to enter monthly contributions, expected inflation and growth rates to estimate how many coins they would need over five to ten years. Results change significantly with price assumptions and withdrawal rules.

Public pension funds have increased indirect exposure to Bitcoin through U.S.-listed strategy vehicles. The New York State Common Retirement Fund and the Texas Teachers pension have added positions in Strategy, formerly known as MicroStrategy, as a proxy for Bitcoin exposure. Pension plans in Ohio, California through CalPERS and Louisiana have disclosed similar holdings. Some funds recorded short-term losses tied to public-company volatility but retained allocations as part of medium-term plans. Regulatory changes in the U.S. have expanded the options for including Bitcoin in 401(k) and IRA accounts, which could allow larger retirement pools to gain exposure under formal approval processes and long time horizons.

The asset’s history shows large drawdowns. Bitcoin has fallen more than 70% during past cycles, a level of volatility that affects planning for predictable retirement income. Trader Peter Brandt flagged a potential investable low around September to October 2026 in public posts, a view that other analysts have echoed in warning of cyclical lows before a next sustained uptrend.

Financial advisors report recommending small allocations for investors close to retirement, with some advisory publications suggesting no more than 1% to 5% of a retirement portfolio, adjusted for individual risk tolerance. Exposure-management strategies cited by advisors include long-term holding, using Bitcoin as collateral for loans to generate liquidity without selling, and flexible withdrawal rules that reduce distributions in down years. Rajat Soni, CFA, wrote on X that “Bitcoin is perfect for long-term savings. But don’t sacrifice everything for the future. Make sure you also invest in the present.”

For those planning around a 2030 retirement date, the variables most frequently identified by market participants are price trajectory, chosen withdrawal rate, and the investor’s capacity to absorb large short-term losses. Institutional adoption and divergent price forecasts widen the range of scenarios in which 2 to 5 BTC could support a $100,000 annual income, while volatility and timing risk remain factors cited by advisors and analysts.

Articles by this author